VWAP Trading Mastery

Volume Weighted Average Price (VWAP) is the single most important indicator for institutional traders. It represents the true average price weighted by volume throughout the trading session.

What is VWAP?

Calculation

- VWAP = Cumulative (Price x Volume) / Cumulative Volume

- Resets at the beginning of each trading session

- Gives more weight to price levels where more volume traded

- Represents the "fair price" for the session

Why Institutions Use VWAP

- Benchmark for execution quality

- Buying below VWAP = good execution

- Selling above VWAP = good execution

- Many institutional algorithms are designed to execute at or near VWAP

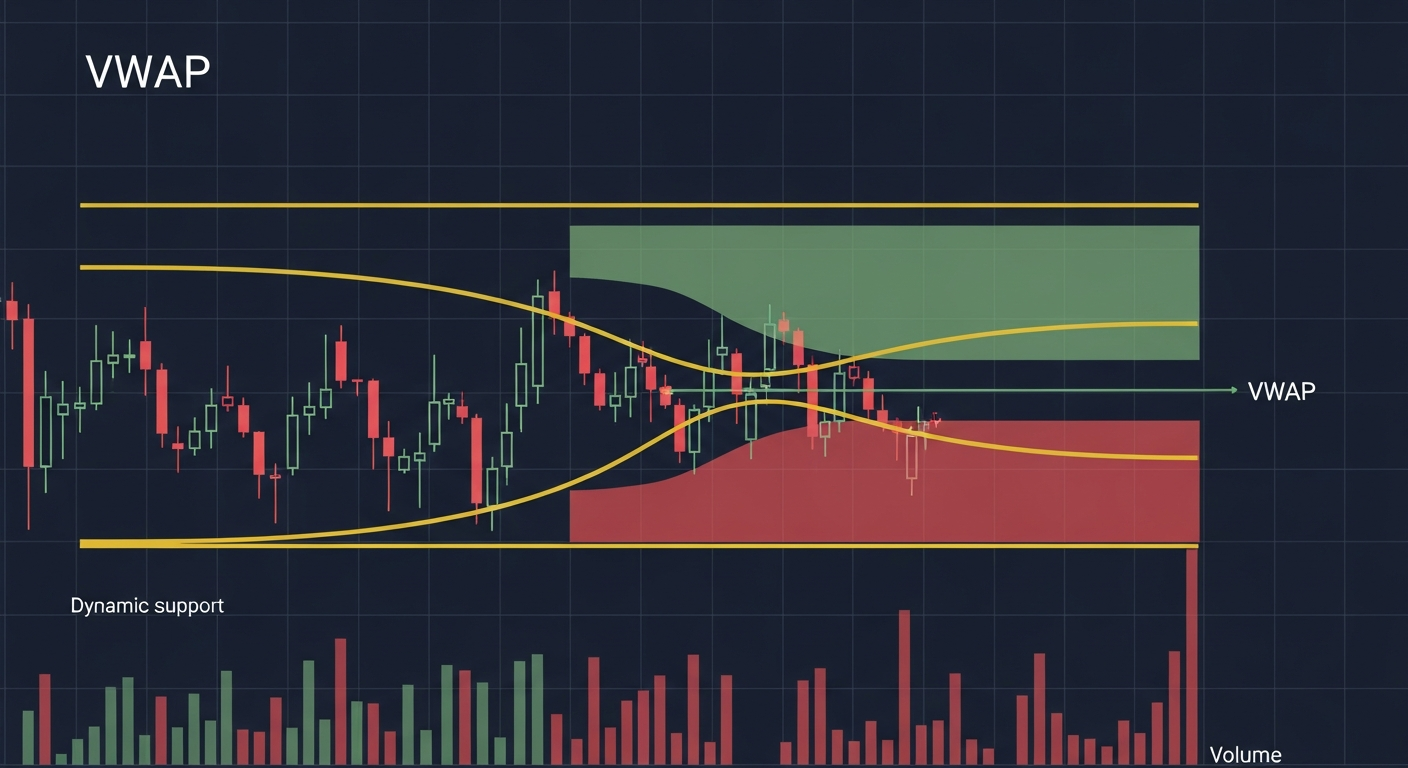

VWAP as Dynamic Support/Resistance

In an Uptrend

- Price stays above VWAP throughout the day

- Pullbacks to VWAP are buying opportunities

- VWAP acts as dynamic support

- As long as price respects VWAP from above, the trend is intact

In a Downtrend

- Price stays below VWAP throughout the day

- Rallies to VWAP are selling opportunities

- VWAP acts as dynamic resistance

- The trend is bearish as long as VWAP holds from above

VWAP Standard Deviation Bands

First Deviation (+1 / -1)

- Contains approximately 68% of price action

- Touches are potential mean-reversion entries

- First target when fading extremes

Second Deviation (+2 / -2)

- Contains approximately 95% of price action

- Strong overbought/oversold zones

- High-probability fade zones

- Price reaching second deviation often reverts

Third Deviation (+3 / -3)

- Extreme levels reached only in very volatile conditions

- Almost always reverts at least partially

- Use for aggressive counter-trend scalps

VWAP Trading Strategies

VWAP Bounce Strategy

- Identify the trend direction (price above or below VWAP)

- Wait for a pullback to VWAP

- Look for a candlestick reversal pattern at VWAP

- Enter in the trend direction

- Stop: Beyond the VWAP level (tight stop)

- Target: Recent extreme or deviation band

VWAP Deviation Fade

- Price reaches the second or third deviation band

- Look for rejection candles (doji, hammer, engulfing)

- Enter against the move, targeting VWAP

- Stop: Beyond the deviation extreme

- Best in range-bound or moderate trend days

VWAP Cross Strategy

- Price crosses above VWAP after being below = Bullish shift

- Wait for a pullback to VWAP for entry

- Price crossing below VWAP after being above = Bearish shift

- This works best in the first 2-3 hours of the session

Anchored VWAP

What is Anchored VWAP?

- VWAP calculated from a specific starting point instead of session start

- Anchor from: Earnings, significant highs/lows, IPO date, news events

- Shows the average entry price from that key event

- Institutional positions are often referenced to these levels

How to Use

- Anchor from the most recent major swing low (for support)

- Anchor from the most recent major swing high (for resistance)

- Multiple anchored VWAPs can create confluence zones

VWAP for Different Markets

Stocks

- Resets daily (session VWAP)

- Most effective in the first 2-3 hours

- Less useful in the last hour (anchoring effect diminishes)

Forex

- No official "session" so anchor to key sessions (London open, NY open)

- Weekly VWAP is popular for swing trading

- Less common but still effective

Crypto

- 24/7 market so weekly or custom VWAP works best

- Anchored VWAP from major highs/lows is very effective

Key Takeaways

- VWAP is the institutional benchmark, use it as your reference

- Price above VWAP = bullish bias, below = bearish bias

- Deviation bands provide mean-reversion opportunities

- Anchored VWAP from key events reveals institutional cost basis

- VWAP is most effective in the first half of the trading session

Lesson Discussion